For private foundations and public charities, the investment policy statement is crucial

Board-approved documents outlining financial goals and investment objectives guide endowments and foundations through volatile markets. Here are some tips from Bank of America.

The market conditions that characterized 2022 demonstrated in a clear way the value of an investment policy statement (IPS). The year 2022 was an exceptionally trying period, as surging inflation, the economic dislocations that accompanied the Russian invasion of Ukraine, and a bear market in equities combined to cause declines in the value of the endowments that private foundations and public charities depend on to fund grantmaking and operations.

In many cases, having an IPS — which sets out policies, procedures and guidelines for managing the endowment’s investments, among other factors — helped organizations and their board members resist the urge to make rash decisions in the heat of the moment. “The IPS is a refuge for rationality in times of turbulence,” says William Jarvis, a managing director and philanthropic executive for Bank of America.

But an IPS isn’t useful only when markets are volatile. This foundational document records the organization’s investment approach and mission statement in a single, accessible place. For a new board trustee or investment committee member, reading the IPS should serve as a crash course in how the nonprofit’s investments support its objectives and how they are to be managed and spent. Here are some ideas from Bank of America for how to get started with creating — or updating — an IPS for your organization.

Start with your mission

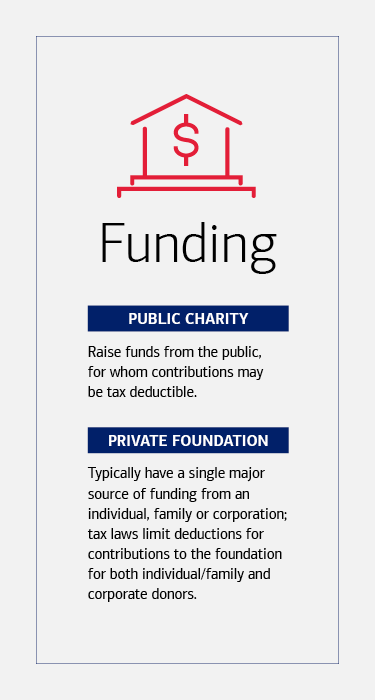

Creating an IPS begins with spelling out the purpose of the organization’s endowment. “Money serves mission,” says Jarvis. For private foundations, typically established and run by individuals, families or corporations, that means identifying the charitable goals that are to be accomplished and meeting the legal requirement that they spend at least 5% of the value of their assets annually, generally through making grants to other nonprofits. Public charities have more flexibility, and spending may vary from year to year; in some years, this kind of nonprofit may decide not to spend from its endowment.

Match investment return goals with spending needs

Next, the IPS needs to set a target for investment returns. Apart from the 5% minimum that private foundations must spend, public charities spend an average of about 4.5% of their assets each year, and the endowment needs to generate a return that can cover those expenditures. “But an organization’s board and its other fiduciaries have an additional legal responsibility,” says Jarvis. “They need to ensure that the endowment maintains its inflation-adjusted purchasing power over the long haul.”

That means adding an estimate of long-term inflation to the investment target. Until recently, most organizations used 2%, and even though prices have risen at a much faster rate, a figure of 3% may be reasonable as a projected average over the next 15 to 20 years, Jarvis says. Adding 3% to 4.5%, with an additional 1% to cover the costs of investment management, might bring the return target to 8.5%.

That target is the return, on average, that the endowment’s investments need to earn. But for the organization’s fiduciaries, determining how to invest those funds also means considering the risks that may affect investment performance. “Risk is often thought of as volatility — how much returns may fluctuate,” says Jarvis. “But there are also other kinds of risk — of capital loss and liquidity, risks to an organization’s reputation and quantitative measures of risk that can help you see how much risk you’re assuming with a given investment, bearing in mind that it is the total risk, at the portfolio level, that is most relevant over time.” All of those, articulated in the IPS, help guide the organization’s investment strategy.

Agree on investment types

Then there is the matter of what kinds of investments are approved or prohibited. Some organizations will choose to stick with traditional assets such as U.S. stocks and investment-grade bonds, perhaps adding international equities, says Jarvis. Other nonprofits, particularly larger ones, may be willing to consider hedge funds, real estate, private equity and other investments that can serve to broaden diversification.

But the mission and values of an organization may also affect what assets are considered suitable or off limits. “To take one example, a private family foundation may feel that its values need to be expressed through the portfolio," Jarvis says. A board's decision to adopt criteria for its investment portfolio might require acknowledgment in the IPS.

Align asset allocations

Based on all those factors — the endowment’s purpose, its investment target, the approach to risk and approved and prohibited investments — as well as the need for liquidity to fund spending goals, the IPS will specify a target asset allocation for the endowment. “There need to be ranges around which the individual allocations are permitted to move as markets move,” says Jarvis. So, for example, a 20% allocation to a particular asset might be allowed to go as high as 30% or as low as 10%. When allocations go above or below those ranges, investment managers will rebalance, buying or selling assets to bring the portfolio back to within its target range.

Revisit on a regular basis

Once a nonprofit has developed its investment policy statement, it should be reviewed every year. And because an organization’s board members and other fiduciaries, who are legally responsible for the entity’s endowment, may not be experts in portfolio construction and management, most nonprofits choose to work with financial professionals such as those at Bank of America who can guide the process of establishing and implementing investment policies.

“When Bank of America works with a new organization, reviewing or creating an IPS is one of the first things we do,” Jarvis says. “We talk with them about their mission, and then we help them to incorporate their goals into this document.” Then the investment managers can use the IPS as a blueprint for meeting those objectives, in both calm and turbulent financial markets.

A Private Wealth Advisor can help you get started.

Disclosure:

Donor-advised fund and private foundation management are provided by Bank of America Private Bank, a division of Bank of America N.A., Member FDIC and a wholly owned subsidiary of Bank of America Corporation.

Institutional Investments & Philanthropic Solutions (also referred to as “Philanthropic Solutions” or “II&PS”) is part of Bank of America Private Bank, a division of Bank of America, N.A., Member FDIC and a wholly owned subsidiary of Bank of America Corporation (“BofA Corp.”). Trust, fiduciary, and investment management services are provided by wholly owned banking affiliates of BofA Corp., including Bank of America, N.A. and its agents. Brokerage services may be performed by wholly owned brokerage affiliates of BofA Corp., including Merrill Lynch, Pierce, Fenner & Smith Incorporated (also referred to as “MLPF&S” or “Merrill”).

MLPF&S makes available certain investment products sponsored, managed, distributed or provided by companies that are affiliates of BofA Corp. MLPF&S is a registered brokerdealer, registered investment adviser, Member SIPC and a wholly owned subsidiary of BofA Corp.